Everything you need to know about accounting.

“Life is like accounting, everything must be balanced”

Accounting is a very interesting yet difficult subject. It is not just about profit, money or numbers it is also about decision making, problem-solving, situation analysis, and control. Accounting is done by almost everyone in our everyday lives.

You go to the supermarket to buy snacks. You have Php 105. How best can you utilise the Php105 for your satisfaction?

You were given pocket money every week by your parents. You see this amazing laptop on the market. You calculate how much you need to save and how many weeks it will take to buy the laptop. You budget.

What is Accounting?

Accounting is the systematic and comprehensive recording of financial transactions pertaining to a business. Accounting also refers to the process of summarizing, analyzing and reporting these transactions to oversight agencies, regulators and tax collection entities.

The Basic Model of Accounting : Assets = Liabilities + Equity

An asset is a resource with economic value that an individual, corporation or country owns or controls with the expectation that it will provide a future benefit. Assets are reported on a company’s balance sheet and are bought or created to increase a firm’s value or benefit the firm’s operations.

Two types of Assets

Current assets are short-term economic resources that are expected to be converted into cash within one year. Current assets include cash and cash equivalents, accounts receivable, inventory, and various prepaid expenses.

Non-Current Assets long-term resources, such as plants, equipment, and buildings. An adjustment for the aging of fixed assets is made based on periodic charges called depreciation, which may or may not reflect the loss of earning powers for a fixed asset.

A liability, in general, is an obligation to, or something that you owe somebody else. Liabilities are defined as a company’s legal financial debts or obligations that arise during the course of business operations.

Two types of Liabilities

Current Liabilities are a company’s debts or obligations that are due within one year or within a normal operating cycle. Furthermore, current liabilities are settled by the use of a currentasset, such as cash, or by creating a new current liability.

Non–current liabilities are long-term liabilities, which are financial obligations of a company that will come due in a year or longer.

Owner’s equity represents the owner’s investment in the business minus the owner’s draws or withdrawals from the business plus the net income (or minus the net loss) since the business began. Owner’s equity is viewed as a residual claim on the business assets because liabilities have a higher claim.

The Accounting Cycle/Process

Transaction Analysis (Step 1)

The analysis of transactions should follow these four basic steps 1. Identify the transaction from source documents 2.indicate the accounts-either assets,liabilities, equity, income or expenses affected by the transaction. 3. Ascertain whether each account is increased or decreased by the transaction. 4. Using the rules of debit and credit, determine whether to debit or credit the account to record increase or decrease

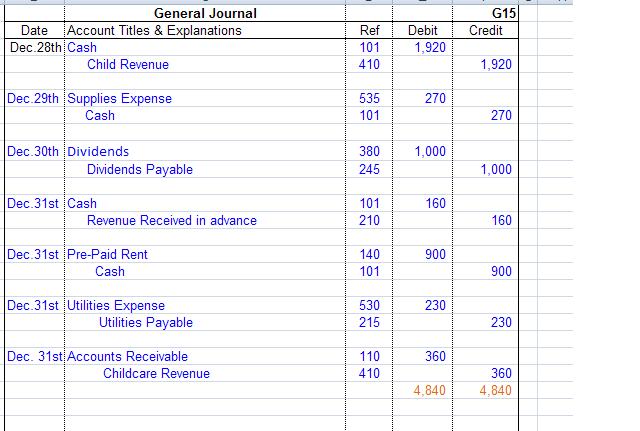

Transaction are Journalized (Step 2)

After the transaction or event has been identified and measured, it is recorded in the journal. The process of recording a transaction is called journalizing.

Posting (Step 3)

Posting means transferring the amounts from the journal to yhe appropriate accounts in the ledger. Debits in the Journal aren posted as debits in the ledger, and credits in the journal as credits in the ledger.

Trial Balance (Step 4)

The trial balance is a list of all accounts eith their respective debit or credit balances. It is prepared to verify thr equality of debits and credits in the ledger at the end of each accounting period or at any time postings are updated.

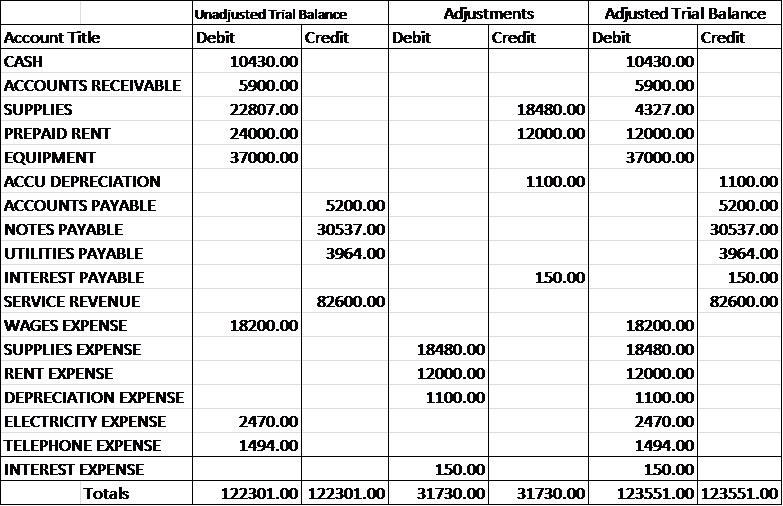

(Step 5) Preparing the worksheet

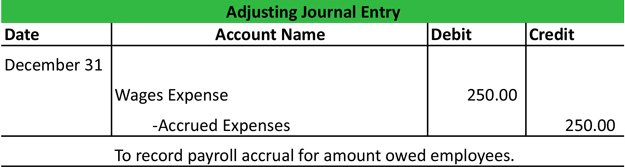

Adjusting entries are journal entries used to recognize income or expenses that occurred but are not accurately displayed in your records. You create adjusting journal entries at the end of an accounting period to balance your debits and credits.

- Enter the account balances in the unadjusted trial balance columns andd total the amounts.

- Enter the adjusting entries in the adjustments column and total the amounts.

- Compute eash account’s adjusted balance. Enter the amounts in the adjusted trial balance.

Step 6: Preparing the financial statements

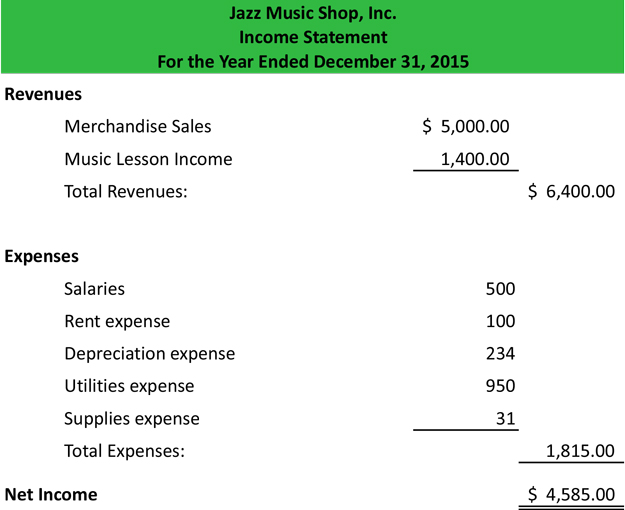

Statement of Income or Income Statement

An income statement is one of the three important financial statements used for reporting a company’s financial performance over a specific accounting period, with the other two key statements being the balance sheet and the statement of cash flows. Also known as the profit and loss statement or the statement of revenue and expense, the income statement primarily focuses on the company’s revenues and expenses during a particular period.

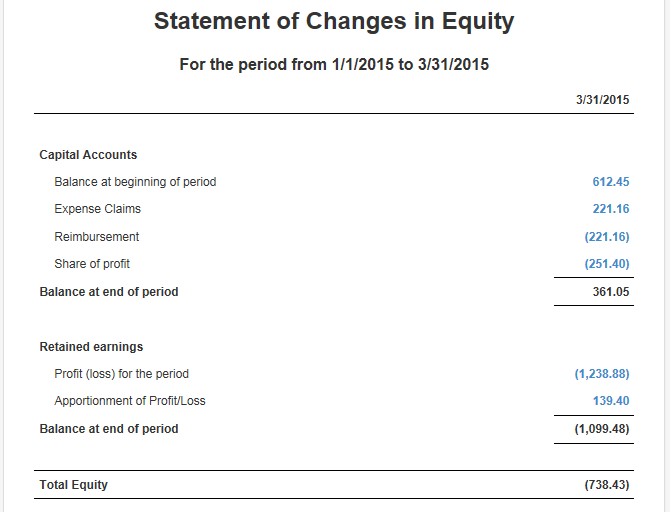

Statement of Changes in Equity

The statement of changes in equity shows the change in an owner’s or shareholder’s equity throughout an accounting period. Also called the statement of retained earnings, or statement of owner’s equity, it details the movement of reserves that make up the shareholder’s equity

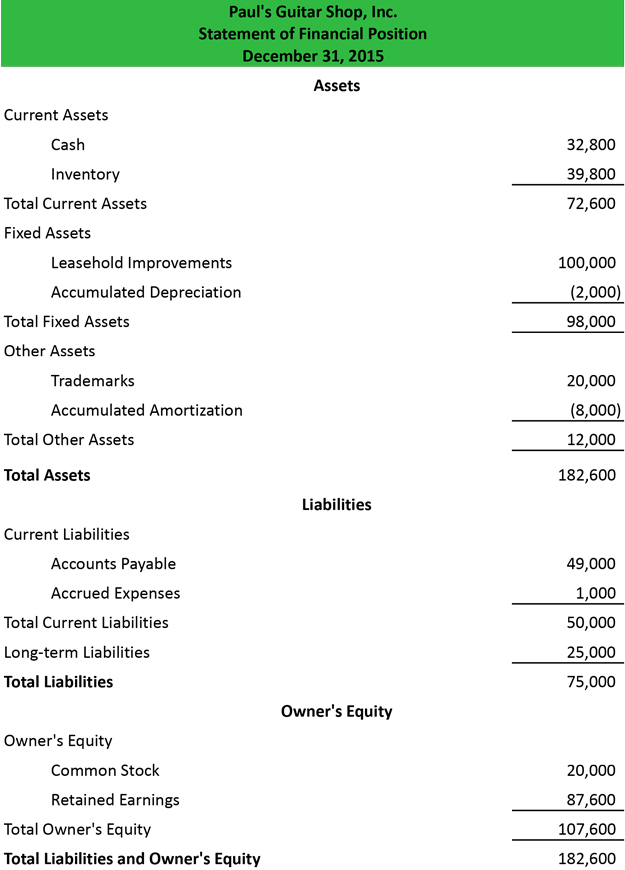

Statement of Financial Position or Balance Sheet

The statement of financial position, often called the balance sheet, is a financial statement that reports the assets, liabilities, and equity of a company on a given date. In other words, it lists the resources, obligations, and ownership details of a company on a specific day.

Step 7: Adjustments are journalized and posted

The adjustment process is a key element of accrual basis accounting. The worksheet helps in the identification of the accounts that need adjustments. The adjusting entrries are directly entered in the worksheet. Most accountats prepare the financial stements immediately after completing the worksheet. The adjustments are journalized and posted as the closing entries are made. This step in the accounting cycle brings the ledger into agreement with the data reported in the financial statements.

Step 8: Closing entries

Closing Entries are journalized and posted Income, expense and withdrawal accounts are temporary accounts that accumulated information related to a specific accounting period. These temporary accounts facilitate income statement preparation. At the end of each year, the balances of these temporary accounts are transferred to the capital account. Thus, the balance of the owner’s capital account represents the cumulative net result of income, expense, and withdrawal transactions. This phase of the cycle is called the closing procedure.

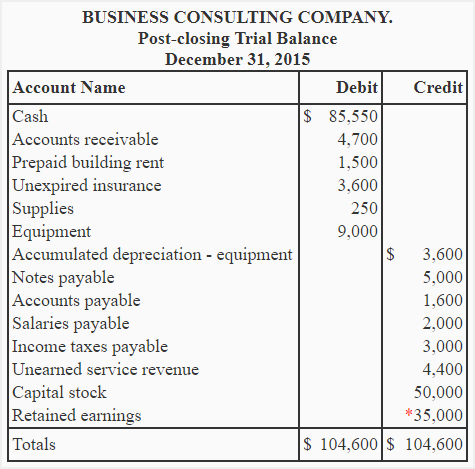

Step 9: Preparation of a post-closing trial balance

It is possible to commit an error in posting the adjustments and closing entries to the ledger accounts; thus, it is necessary to test the equality of the accounts by preparing a new trial balance. This final trial balance is called a post-closing trial balance.